Edition 20: Making sense of a bumpy ride

Top of the news

Non-fungible tokens (NFTs) have taken off with Twitter’s Jack Dorsey auctioning his first tweet, currently at $2.5MM; a digital album from American DJ 3LAU sold for $3.6MM, and an authentic Banksy was burned to make way for its digital counterpart, now listed at $112K.

Oil prices have climbed as a result of OPEC limiting supply; the average price in the United States for a gallon of regular gasoline is now $2.77, according to AAA, up from $2.46 a month ago.

According to Redfin, the average sale-to-list price ratio, which measures how close homes are selling to their asking prices, increased to 99.6%—1.6 percentage points higher than a year earlier and an all-time high. Meanwhile, lumber prices have soared 140% over the last year.

The Treasury 10-year note yield climbed to 1.568%, the highest it has been since Feb 2020. The 30-year mortgage rate has also exceeded 3%. The S&P 500 is down 1.8% on the month.

SPACs have also gained popularity as “blank check” acquisition companies that help startups quickly list on stock exchanges, sidestepping many standard IPO SEC requirements. Luminar Technologies, which makes lidar for autonomous vehicles, Virgin Galactic, Clover Health and Lion Electric have recently gone public through SPACs.

Van Eck Vectors Social Sentiment ETF ($BUZZ) launched on the heels of the WallStreetBets/Reddit mania around $GME, which is now trading at $137.74. It includes “75 large cap U.S. stocks which exhibit the highest degree of positive investor sentiment and bullish perception based on content aggregated from online sources including social media, news articles, blog posts and other alternative datasets”. Its biggest holding by share is Ford.

Why did the Treasury bond yield climb?

It’s worth remembering that bonds don't necessarily have prices as stocks do; they have yields. They promise a rate of return on every dollar borrowed from the buyer. When the bond yield climbs, it reflects increased demand which means investors expect the return on these (the interest rate) to increase.

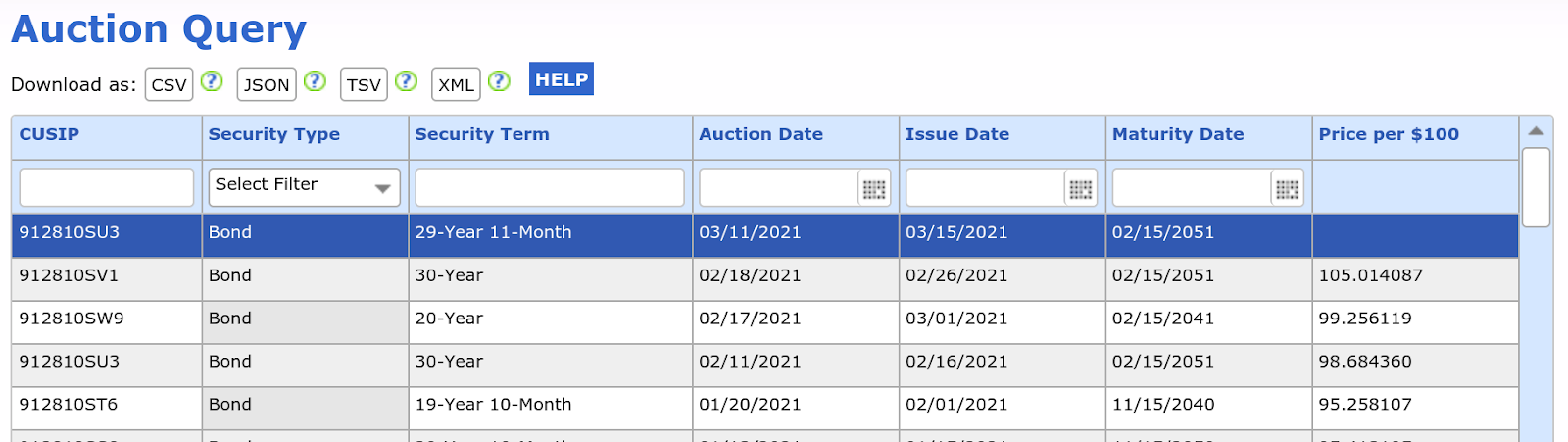

In the screenshot below, you can see that the auction for US Treasuries on the 18th saw the price per $100 exceed 100, which means you’re actually paying more for the Treasury than it’s worth. Explore more here.

Why does this affect mortgage interest rates?

The short answer is that investors believe a faster recovery from the pandemic means increases in interest rates for borrowing money at a pace sooner than the Feb claims it will.

Bonds are exchanged on the market just like stocks are, and market demand for them sets the price upwards or downwards. (Government bonds are issued via ETFs but can also be bought directly). With the pandemic, most investors saw governments minimize or eliminate interest rates for borrowing for individual and small businesses to stimulate the economy, making long-term debt borrowing less attractive.

The Federal Reserve (and central banks in most countries) play a key role in encouraging lower interest rates (unlike Congress, the Fed cannot pass laws to require low interest rates). They do so by buffering the purchasing prices for bonds by periodically purchasing bonds or selling them. For example, where local governments might put up bonds in order to finance the repaving of your potholed-filled street, the Fed can purchase those bonds, returning much-needed cash to the economy. The act of purchasing bonds means investors see lower risk (and thus lower reward) for bonds.

A similar but detached bond market sets mortgage rates. Issuers like Ginnie Mae and Freddie Mac interface with banks offering mortgages and sell bundles of mortgages with what are known as mortgage-backed securities on the open market (you can through ETFs: GNMA and MBB; note that the price of the ETF and the underlying bond goes down because there is less demand for bonds if people assume interest rates will increase -- and should therefore buy at a later date). If one bond market (e.g. the Treasury one) prices in interest rate increases, the others (e.g. the mortgage one) tend to follow suit: these are long-term debt notes, after all). Interest rate increases for mortgage backed securities on the bond market means increased interest rates for banks issuing those mortgages, which then pass on those increases to individuals like you and me.

How are interest rates and inflation connected?

Healthy economies factor in an inflation rate of around 2%; this gives ample room for central banks to stimulate the economy while ensuring the average household can expect that prices for their wages will grow (and it also encourages spending, since at a 2% inflation rate $1 today is worth 98 cents on average a year from now). The current concern is that a sudden re-opening of the economy after the pandemic is “over” will drive up higher-than-usual consumption (Hawaii here we come?), encouraging businesses to increase prices of items as demand surges.

The way in which inflation is reigned in is by setting a target federal funds rate (which then has the trickle-down effect on mortgages as well as overall consumer borrowing), as well as repurchasing bonds. If the Fed fund rate increases, people are less incentivized to borrow because it costs more to pay back, and in theory user demand for purchasing items goes down.

And the problem is that the Fed fund rate is currently set to target between 0 and 0.25, in order to stimulate spending. It can only stay low or go up (in some economies, the central bank can reduce interest rates to below 0, where it costs money to store money in banks, but the U.S. has no plans to do so, apparently). The market is basically expecting the Fed to increase the fed fund rates soon, something Fed chair Jerome Powell dismissed earlier this week.

Why are stocks affected?

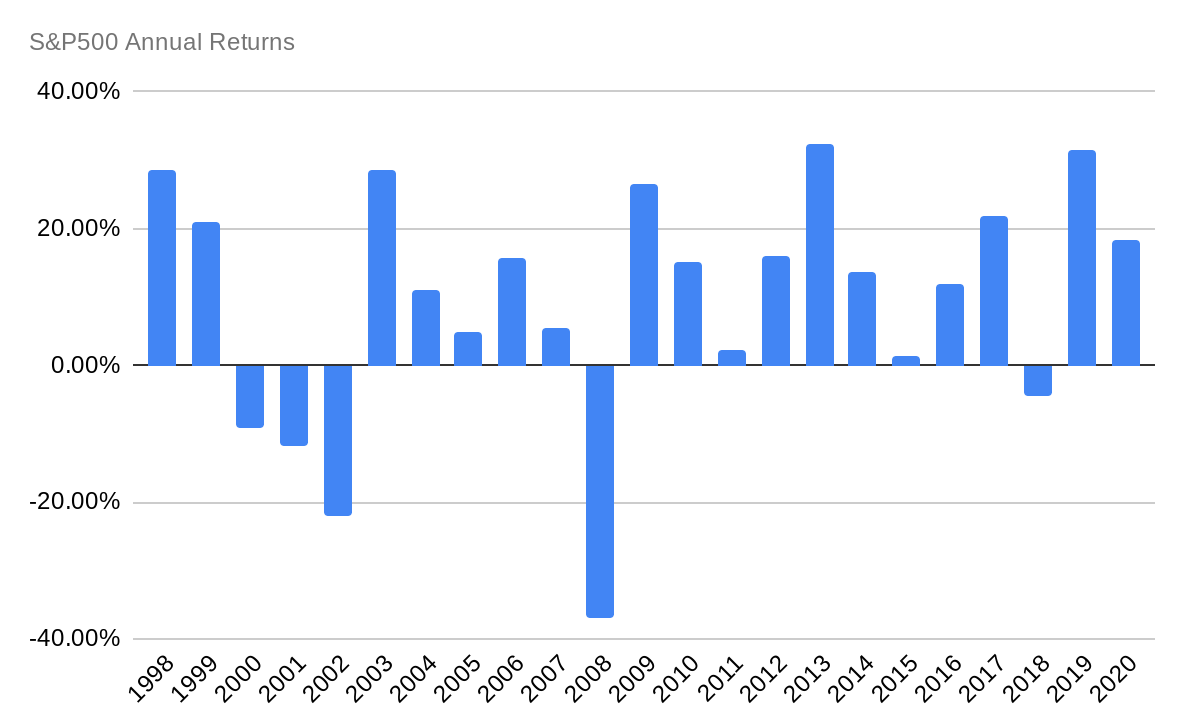

Investors can choose to put their dollars into stocks and bonds (or real estate, for that matter), but a finite amount of money means increasing your bond allocation means shifting money away from stocks. With 2020’s S&P annual returns at 18.40%, investors are considering shifting their profits into safer allocations. The other side of the equation impacts the underlying stock itself: if the fed funds rate does increase, the price of borrowing eats into corporate profits, decreasing earnings per share (interestingly, it appears though historically that the Fed increasing rates is correlated with stronger underlying economic scenarios, and the S&P 500 performs better)

Is there any reason to worry? The only one I have is that rampant speculative instruments like SPACs (according to Spac Alpha, some 187 S-1s were filed in February alone, nearly double that of January), new modes of investment like NFTs and cryptocurrency smells a lot like the way things were prior to the 2000 dot-com bust (see above). Most analysts appear to converge on the idea that the underlying technology assets are far more robust than they were 20 years ago (except, perhaps, Michael Burry), but the impatience I see with people wanting quick returns on the cash sitting in their bank accounts makes me worried there isn’t sufficient due diligence being conducted. Market manipulation, crypto scams (one just happened last week), broker fraud (remember Quadriga and OneCoin)... nothing seems unlikely to repeat itself now.

What’s next?

Let’s play out the scenario further, shall we?

Bond yields and mortgage rates could continue to rise. The primary beneficiary of this are financial institutions like banks, because without further Fed action the funds rate remains low while mortgage rates are higher. Current analyst expectation is that the bond yield growth won’t be sufficiently large enough to require Fed intervention.

Inflation probably will kick up but it may be a temporary one. With the latest $1.9 trillion stimulus package and unprecedented savings stored in banks, pent-up demand likely means a “hot” economy in the quarters to come. The prices for items in your local business may have increased because of the pandemic, and are likely to stay there (my local bakery’s kouign amman is now $5 each, up 11% from a year ago).

The Fed could increase rates sooner than it expected. The current expectation is that rates won’t rise at least through to mid-2022, but that could change.

At the end of the day, though, I’m convinced a long-term view on investments will make this bumpy road look like a tiny blip.

In other news

My recent non-Vanguard/SPY holdings have been fairly poor; shares of AZN, GLD, SLV have all underperformed. I’m saved by my holdings of ICLN, IEIH and SLY. I might increase my shares of SLY.

Next time, I’ll go over ESGs (finally) and why I may or may not have purchased Bitcoin. Happy holding!

Rio

Rio Akasaka is not a registered investment, legal or tax advisor or a broker/dealer. Although best effort is made to ensure that all information is accurate and up to date, unintended errors may occur. Past performance is no guarantee of future returns. Always seek financial advice as needed.

Was this email forwarded to you?