Edition 2: Vo-la-ti-li-ty

Edition 2: Vo-la-ti-li-ty

Top of the news: the stock market and the economy are two different things

In the last edition I wrote about the “small bursts of investor confidence”, and Wednesday was really no exception. The trigger? None other than Trump himself. But I doubt this shimmering shiny feeling will last long: the U.S. government is still in partial shutdown (meaning things like the Commerce Department’s GDP and employment reports won’t be published), oil prices are at a rock bottom -- we’ll talk about why that matters later --, politicians like Mnuchin still don’t know if they love or hate the banks, and Trump still would like to get rid of Powell.

As a bit of an aside, I’ve been keeping an eye out on gold. I actually purchased a bit of GLD (SPDR Gold Trust, a fund which tracks the price of gold) over the weekend, just to see where it goes. Because gold is a physical commodity unlike fiat money (e.g. dollars), it tends to perform well in uncertain market economies -- you see it as GLD prices rose as the 2008 recession wore on. I'll keep reporting on it as I learn more.

I think what you’re seeing in the volatility of the markets is uncertainty. Institutional investors hate uncertainty. But let’s not worry about this for now, and instead take the time to examine our (hypothetical/real) portfolios.

What’s in your basket?

Quick! What’s your ideal stock-to-bond ratio? What is it right now? If you don’t know, please go check -- don’t worry, I’ll wait. If you don’t have stocks yet, do you know what it should be?

I’m going to imagine, for the most part, that you own a stock portfolio of some kind. It’s hopefully a retirement account, but you might also have vested stock from your company. You might even have your own Robinhood/InteractiveBrokers/ETrade/Fidelity/Vanguard/ScottTrade account where you’ve played around with stocks. Let’s imagine these as items in a basket with your name on it. Do you know what kinds of stocks these are?

Knowing this -- regardless of what your current investment state is -- is super important before we consider what to buy or sell. It’s super important when you consider that the most important variable in any stock portfolio is your willingness to tolerate risk.

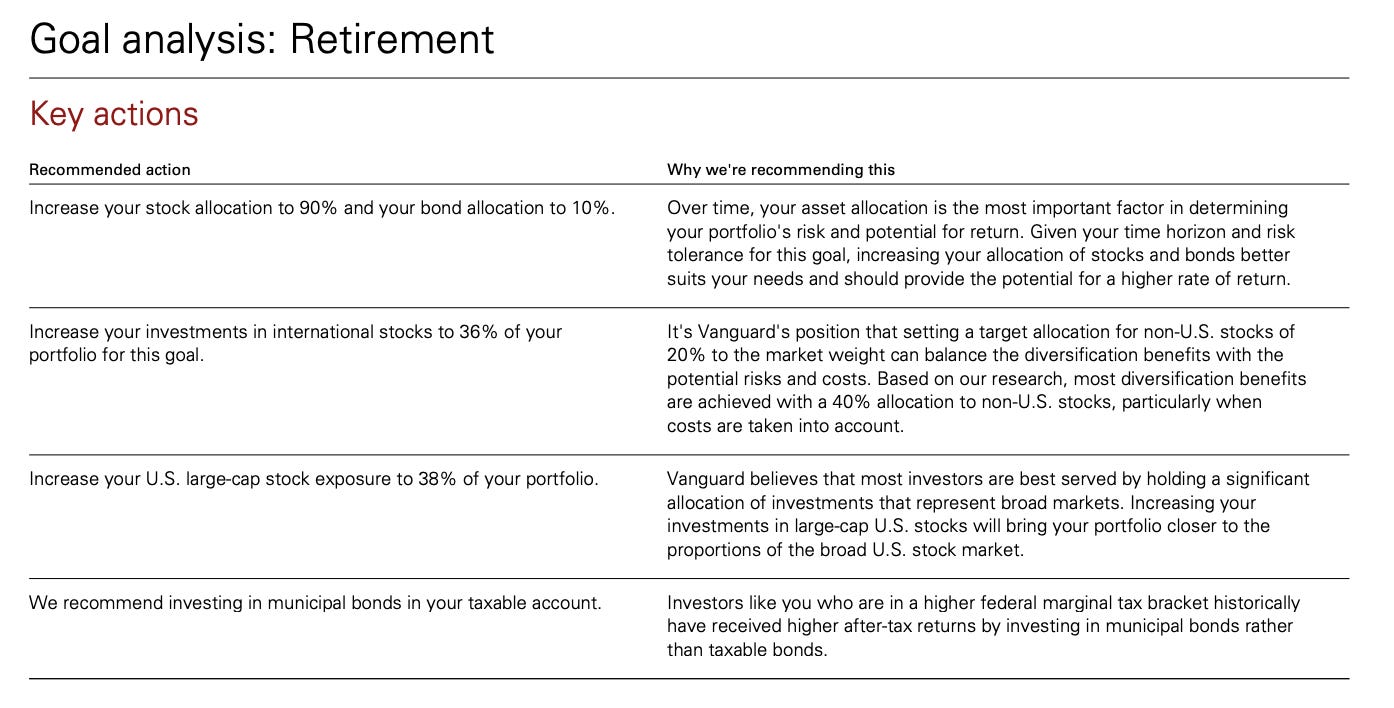

Here’s what Vanguard told me when I opened an account in 2016:

Let’s break the sections down into the four sections as written:

Stocks and bonds

International stocks

Large-cap stocks

Municipal bonds

Vanguard suggests that I should invest 90% of my portfolio -- my basket -- in stocks, and 10% in bonds. Bonds are fancy IOUs offered by governments, and since they are IOUs offered by governments, they provide a rather stable, though relatively unrewarding, return. When you hear or read about the “yield on the 10-year Treasury note”, that’s one kind of bond for which you get the full value of the investment, + interest (currently 2.81%), after 10 years. Stocks are investments in companies (or a basket of companies, or commodities) for which you get regularly rewarded based on performance (dividends), and you can hold onto or resell as you wish. The fact that Vanguard suggests a 90% stock allocation indicates my willingness to tolerate some about of risk and volatility, since stocks can perform well some years/days, or perform miserably others (to be honest, that 90% is a bit too high even for me). You might expect a 8% yearly average return, but you’ll want to be comfortable enough to tolerate a 25% loss on a particularly bad year.

As you get older, and you want more reliable returns on your investments, you expect that stock allocation to go lower and your bond allocation to rise accordingly, reducing volatility and also a bit of your return. Tools like FutureAdvisor can help you simulate your investment returns based on your stock/bond allocation ratio.

If this sounds super basic, not to worry! We’ll go over what stocks to buy, and what those international stocks, large-cap stocks, and alternative investments can look like in a future edition. If you’re feeling like you want to write me, I’d love to hear from you what percentage of your own money you’ve put into stocks.

As an interesting aside, you’d expect that if you loaned the government money for a longer period of time, you’d be rewarded more than if you loaned the government for a shorter period of time -- after all, you can’t quite use that money while it’s loaned. But this is increasingly less true, and when the ratio of 10-year to 1 or 2-year Treasury note yields inverts -- that is, you get less or the same amount of interest if you loan a government for 10 years as you do 1 or 2 -- you have a pretty good indicator that has predicted most of the past recessions. Said another way, the fact that investors won’t want to loan governments money beyond 1- or 2- years means they have reasons to believe the economy won’t be as predictable 10-years down the line. And that’s a slightly worrisome place to be.