Edition 14: Pricing in Uncertainty

Edition 14: Pricing in Uncertainty

One of the most interesting takeaways from the last week has been, besides the election, of course, the fact that the market seems to be increasingly comfortable with uncertainty. And I believe that conflating volatility with uncertainty is a mistake — the future that is uncertain may very well still be a future that is less volatile.

You can actually see below the S&P performance increase with every additional day and more electoral votes assigned; given the Nevada and Arizona time zones I think it is reasonable to conclude that there was almost more information from ballot counts outside of trading hours in NY than there were within trading hours. As of this writing, it has increased 6% since last week.

S&P500 performance over election week

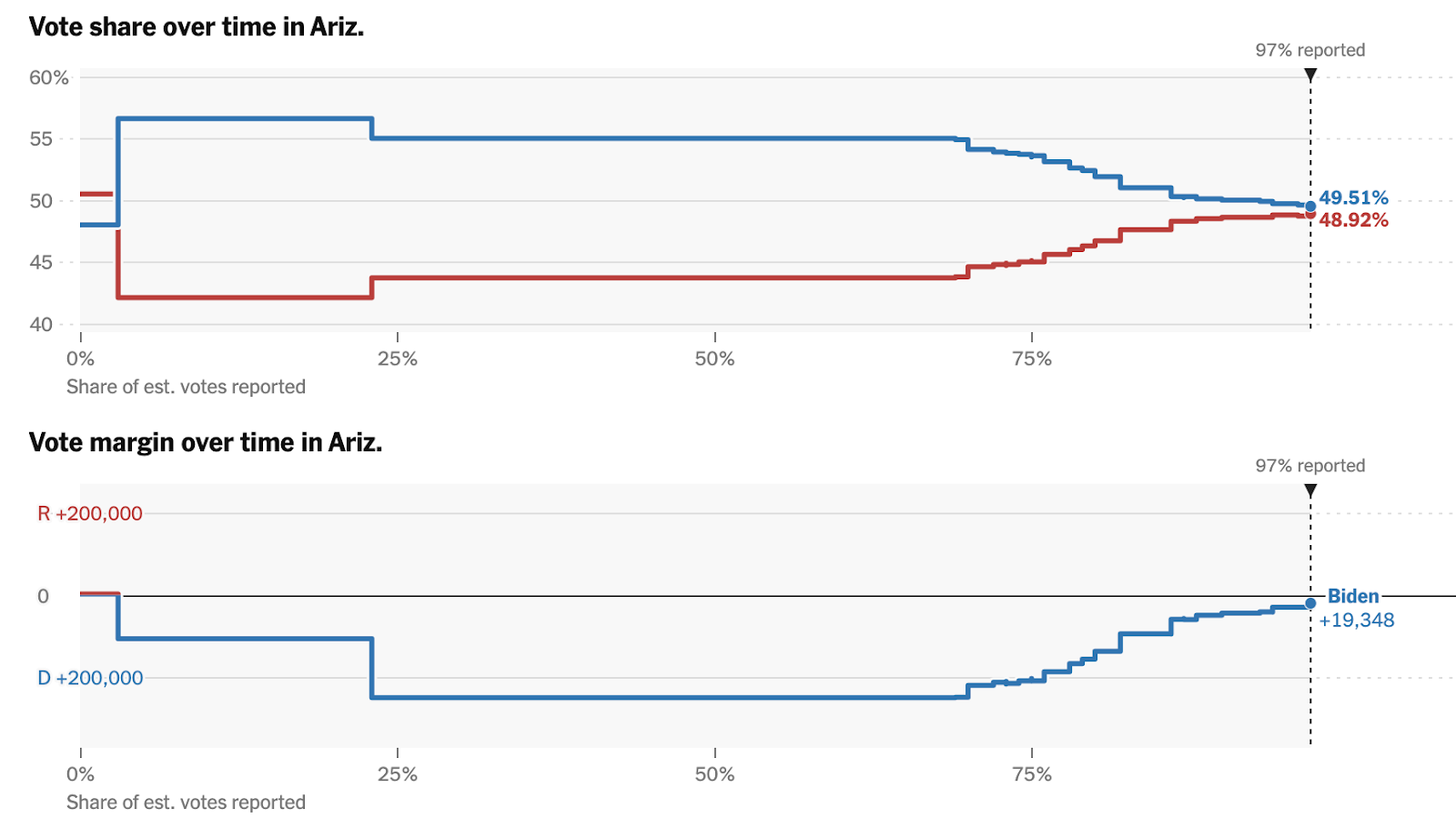

It remains fascinating to observe how much tolerance there is for uncertainty in general, however. For example, the Associated Press called Arizona for Biden at 2:50am on November 4th, while most news outlets, even four days later, have refused to do so. And the margin remains frighteningly close, even with the constant rhetoric that mail-in ballots tend to skew heavily Democratic.

Vote share by party and margin over time for Arizona, as reported by the New York Times

So, what’s next for markets?

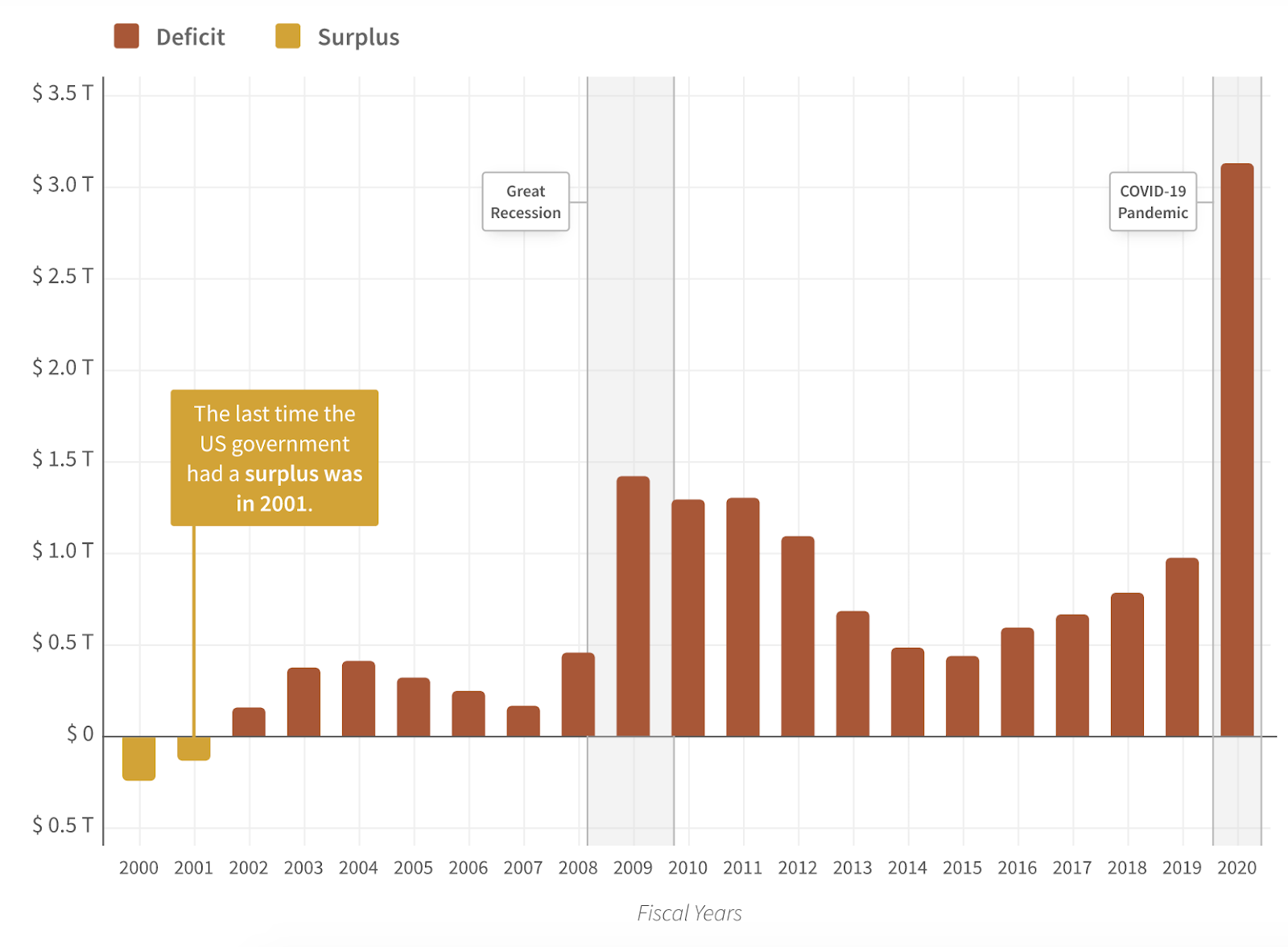

One common refrain we hear is that Trump was great for the economy, having lowered corporate taxes, increased deregulation, reshoring national manufacturing with a trade war (one thing to note: he never did deliver on his promise to spend half a trillion on infrastructure). But reducing the deficit was never part of the agenda, and the U.S now faces a budget shortfall of $3.13 trillion, more than triple the year prior, due in large part to the pandemic.

The U.S. deficit over time; it has been 19 years since the US had a budget surplus

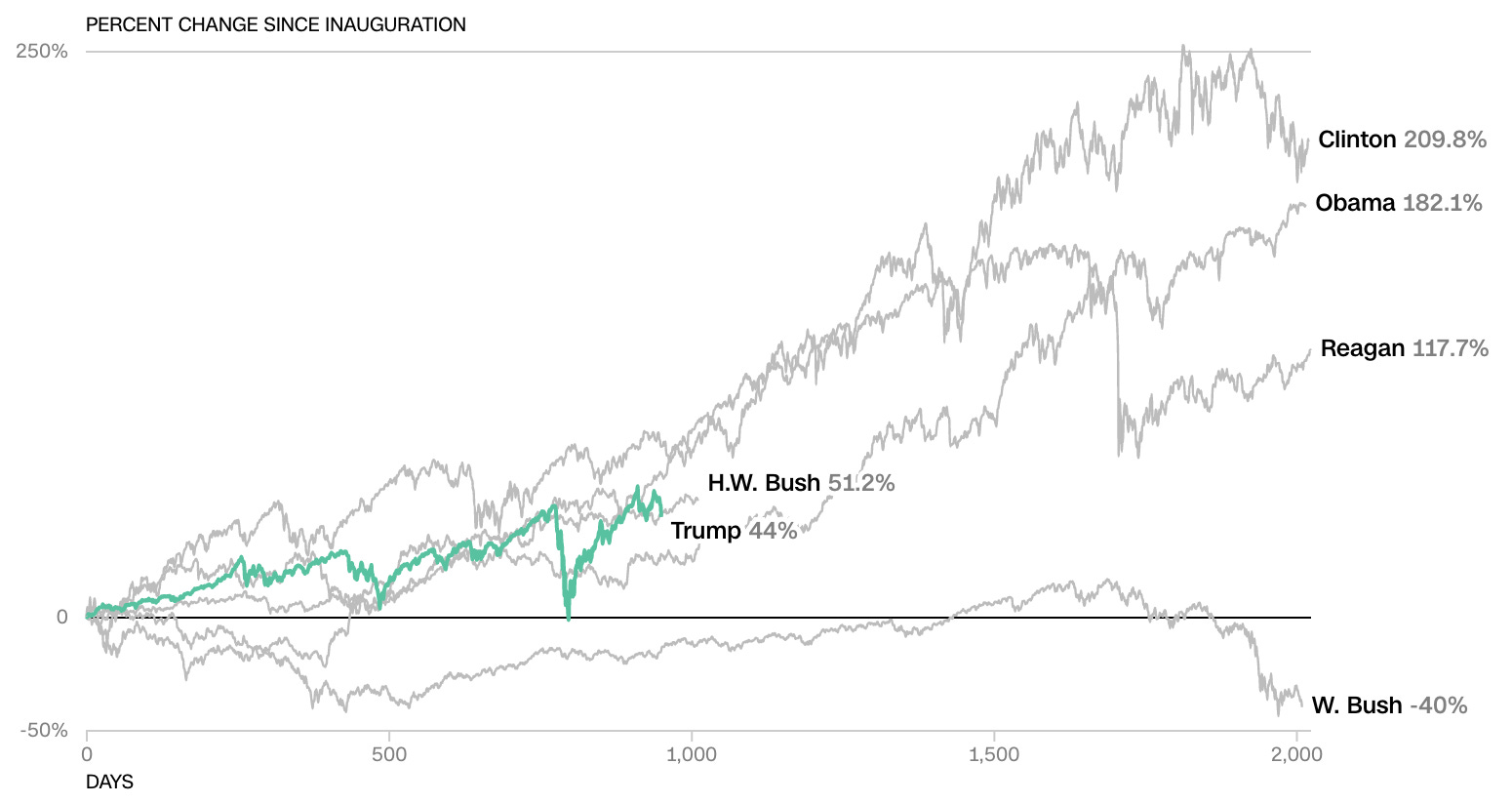

The stock market under Trump’s administration hasn’t exactly been outstanding

With pandemic infection rates spiraling out of control globally and in the United States, more debt in the form of economic stimulus is likely in the short term. Expanding ACA is also expected to increase the deficit even further. It’s very clear that no single policy change can correct the trend (you can try fixing the national debt with some really interesting policy choices here), though reversing some of the corporate and income tax reductions that were made in the Trump era feels inevitable, even if not immediately given the likelihood of a Republican Senate. History does show us that the Democrats are the party of fiscal responsibility.

Winners include clean energy and tech

One very exciting market outcome will be that of renewable and clean energy stocks. ICLN (ESG rating “A”) is the largest clean energy ETF and cheapest in terms of expense ratio; I can’t recommend PBW or TAN due to their limited holdings, lending practices. ICLN’s return YTD is 70%, so admittedly the clean energy train has been running for some time already.

Technology stocks are likely to continue gaining momentum despite ongoing calls for further regulation of the sector, chiefly because the immigration lawsuits and visa headaches that negatively affect hiring and retention will likely be thrown out along with the outgoing administration. (I will note, with some disappointment, the passage of Prop 22, which retains the independent contractor label for gig workers, denying them workers’ compensation, unemployment insurance, family leave, or sick leave). Corporate profits at the expense of the workers they employ seems like a fairly shortsighted calculus.

Re: COVID

The knowns that I mentioned last week still remain however: a vaccine will happen, a stimulus package will happen (when is TBD). But until they do, the virus will continue to wreak havoc on hospital systems as well as local businesses who will struggle to innovate around the challenges of social distancing in the winter. Now is definitely not the time to let our guard down, despite the fatigue and the holidays coming up.

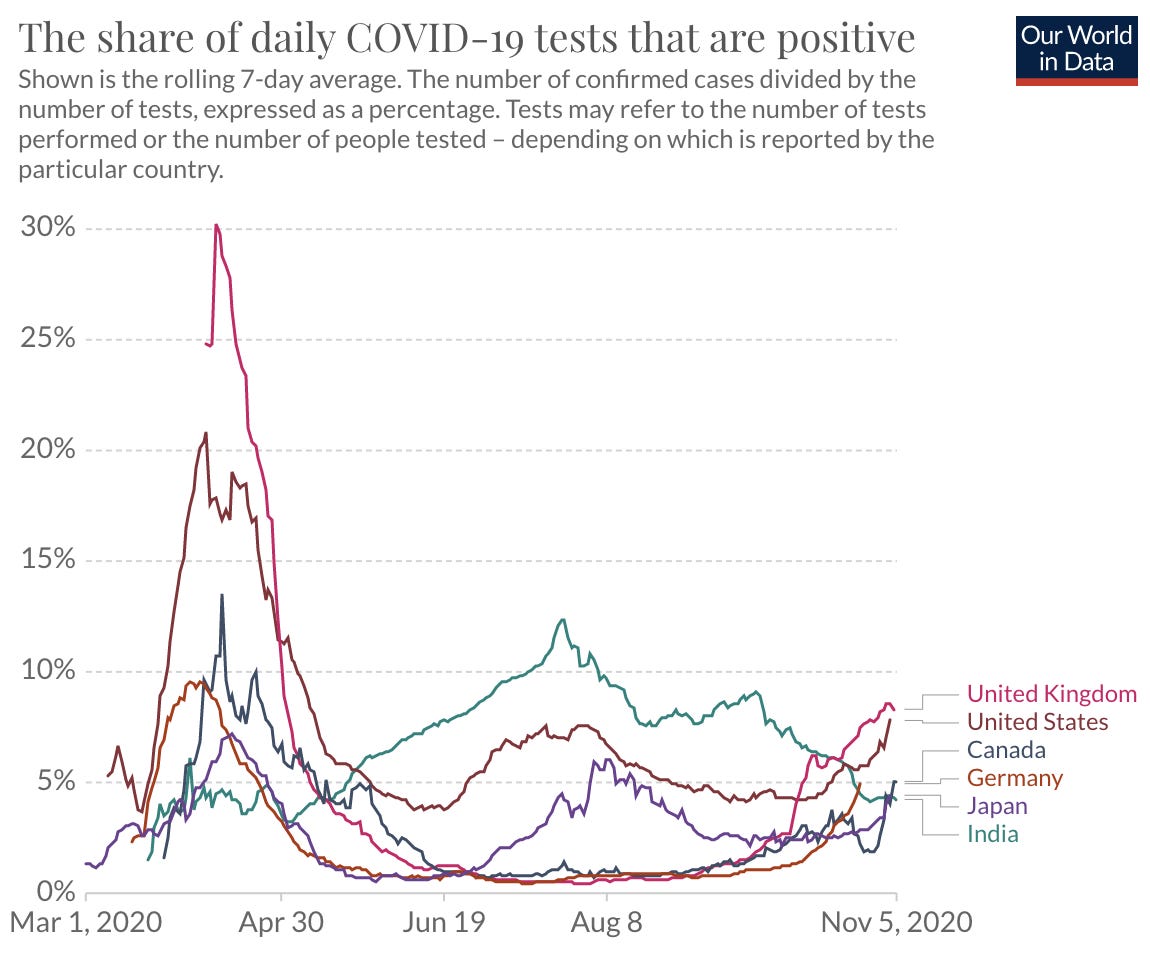

Some of the dashboards that I refer to that aren’t just pure COVID cases or deaths

Summary

Given that the election outcome was nowhere near the Blue Wave that the Democrats had hoped for — the swift and unequivocal repudiation of all of that Trump represented –, there will be much soul-searching, for sure. But one thing is for sure — while Trump revelled in pushing around the stock market with at times impulsive and impetuous tweets at ungodly hours of the morning (see this fascinating study on what happens when he names companies specifically), Biden’s approach to the economy is likely to be more matching of his personality: slow, steady and predictable. And for once, that feels like a great thing.